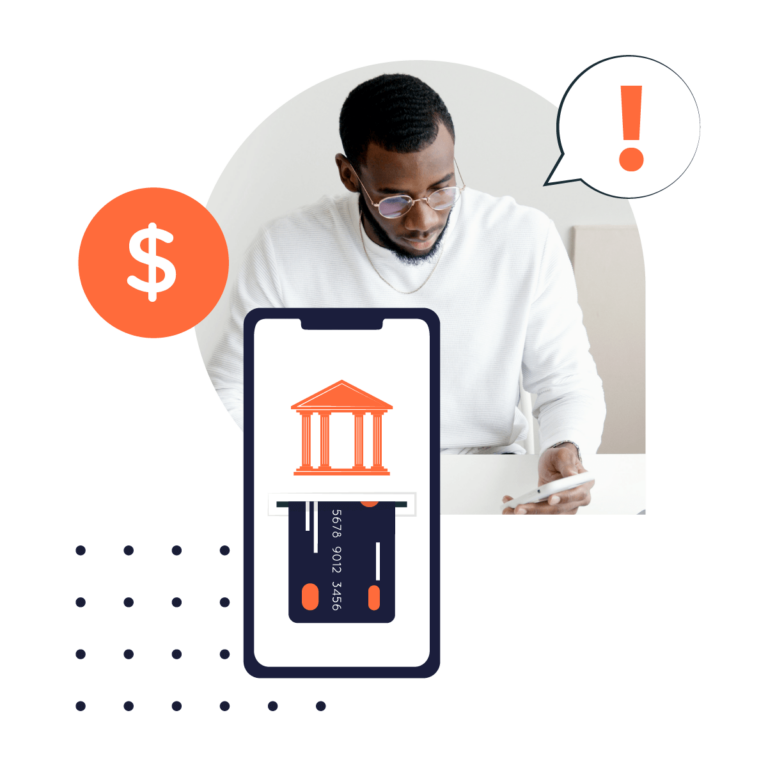

Fight fraud, navigate global financial services regulations and maximize conversions.

Master AML and KYC compliance without compromising on security or customer experience.

Drive trust, not frustration, with seamless, secure onboarding.

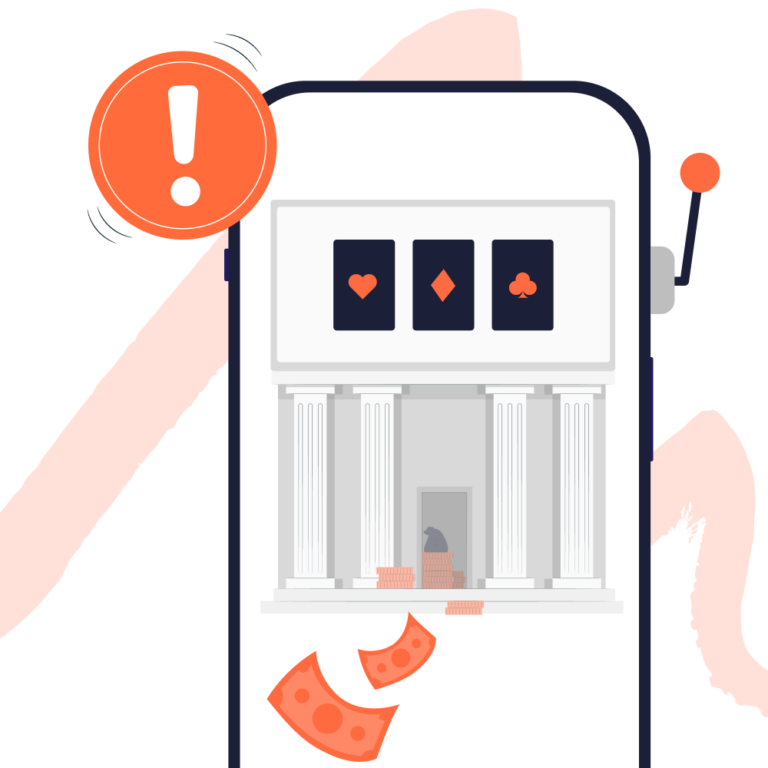

Fight bonus abuse, safeguard against underage gambling and comply with global regulations.

Comply with complex and ever-evolving crypto regulations and combat fraud.

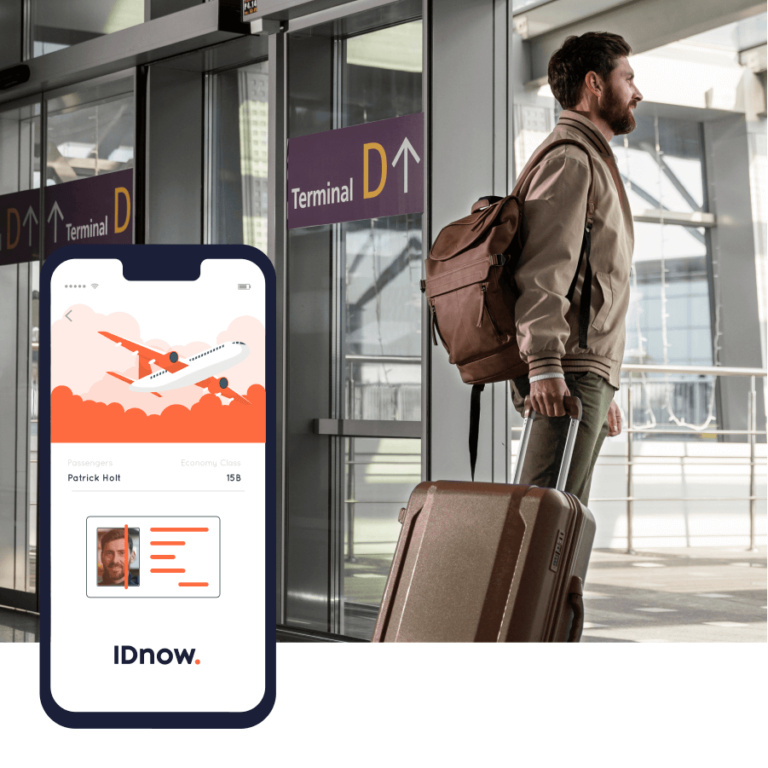

Speed up check-in and travel experiences through secure, seamless onboarding.

Forge trusted telecom connections with secure, streamlined onboarding.

Optimize remote candidate onboarding and protect your business against fraud.

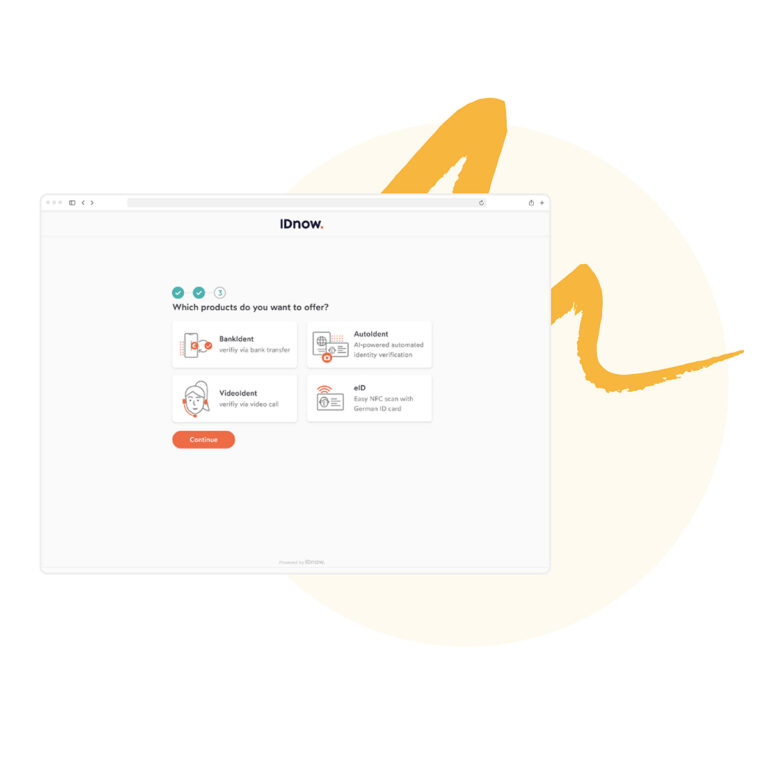

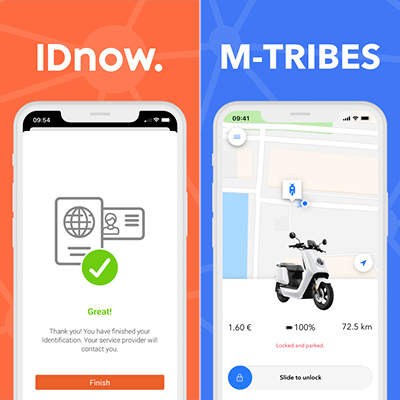

Our automated identity verification solutions enable you to grow and scale your business with confidence.

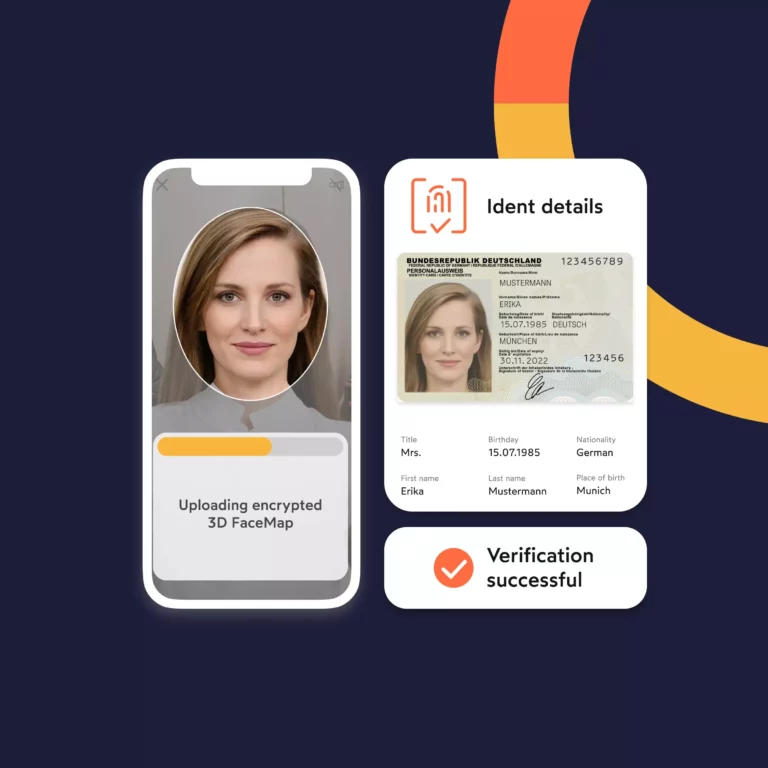

Face-to-face video verification with expert assistance for seamless and secure identity verification.

Offer your customers in-person identity verification at a public location, such as a gas station, near them. Or, perform Point of Sale (POS) identification processes on-site.

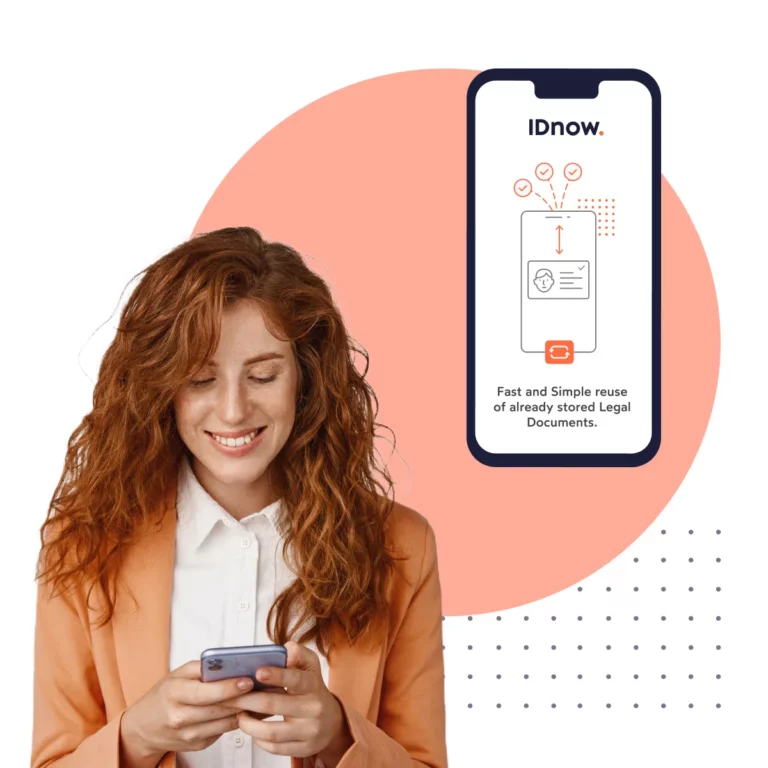

Sign documents easier, faster and more securely without the hassle or cost of paper-heavy processes.

Provides the iOS and Android SDK tools and full API documentation.

Get inspired and stay on top of the latest industry news and insights.

Would you like to get to the bottom of things? We have reports, guides and further insights available for download.

Take a look behind the scenes with our industry case studies available for download.

Our experts keep you up to date on all trends & topics in our webinars.

Our glossary provides up-to-date definitions and explanations.

Access the latest press releases and download IDnow company branding assets.

Become a partner in the global IDnow partnership network.

Check out job opportunities in a fast growing B2B software company in Europe.

Get an impression of the customers around the world who trust IDnow with their identity verifications.

Learn more about the values that guide us as a company.

Learn more about IDnow, the company milestones and meet the management.

Having trouble with your ID verification? Search our knowledge base.

Are you interested in one of our services? Get in touch with our sales team.

Press